Quick Answer

The primary difference between a finance broker vs mortgage broker in Australia lies in their specialisation: a mortgage broker focuses exclusively on property-backed loans (home loans, investment property loans), while a finance broker (also known as a commercial finance broker or business loan broker) assists with a broader range of business financing, including equipment finance, chattel mortgages, and working capital loans. Both are regulated by ASIC and aim to match clients with suitable lenders, but their expertise, lender panels, and product knowledge differ significantly. Businesses seeking asset finance or commercial loans should typically engage a dedicated finance broker or a comparison platform for expert guidance.

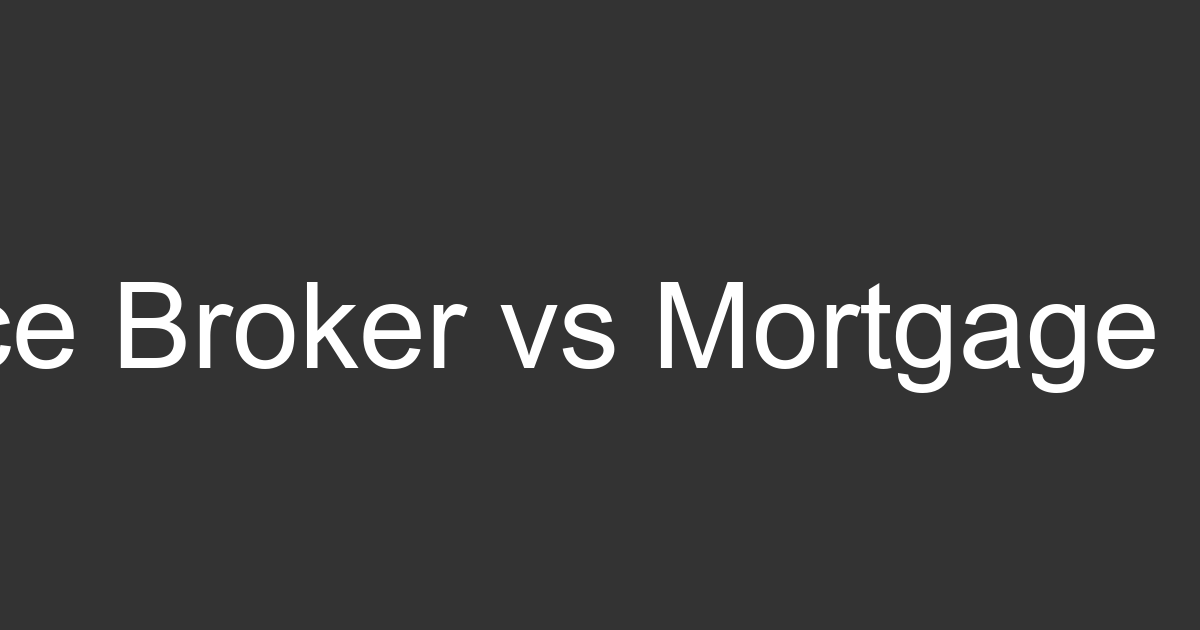

| Feature | Finance Broker (Commercial Finance Broker) | Mortgage Broker (Home Loan Broker) |

|---|---|---|

| **Primary Focus** | Business assets, working capital, commercial loans | Residential & commercial property loans |

| **Product Range** | Chattel mortgages, equipment loans, unsecured business loans, trade finance, invoice finance, vehicle finance | Home loans, investment property loans, refinancing, construction loans |

| **Lender Panel** | Major banks, specialist equipment financiers, non-bank business lenders, private lenders | Major banks, non-bank residential lenders |

| **Expertise** | Business financials, cash flow, tax implications of asset ownership, industry-specific lending | Property valuation, serviceability, LVRs, residential lending criteria |

| **Regulation** | Regulated by ASIC and AFCA (Australian Financial Complaints Authority) | Regulated by ASIC and AFCA |

Rates are indicative examples only. Actual rates depend on individual circumstances and lender assessment.

📄 Navigation Guide

By the Loan Phone team · Reviewed by Anthony Moncada, M.App.Fin, Cert IV Finance & Mortgage Broking, Director

Introduction: Navigating the Broker Landscape

For Australian business owners seeking capital, the terms “finance broker” and “mortgage broker” are often used interchangeably, leading to confusion. However, understanding the distinct roles and specialisations of a finance broker vs mortgage broker is crucial for securing the right funding for your specific needs. While both professionals act as intermediaries between borrowers and lenders, their expertise, product offerings, and even the regulatory frameworks they operate within have important distinctions. This guide clarifies these differences, ensuring you approach the right expert for your business financing journey in 2026. To understand more about why use a finance broker, explore our detailed guide.

What is a Finance Broker?

A finance broker, often referred to as a commercial finance broker or business loan broker, specialises in non-property-backed lending solutions for businesses. Their expertise spans a wide array of products designed to help businesses grow, manage cash flow, and acquire essential assets. These professionals work with a panel of lenders, including major banks, specialist equipment financiers, and non-bank lenders, to find tailored solutions.

Key areas a finance broker typically assists with include:

- Equipment Finance: Securing loans for vehicles (like prime movers, delivery trucks), machinery (excavators, manufacturing equipment), technology, and other business assets through structures like chattel mortgages or hire purchase. Learn more about equipment finance options in Australia.

- Business Loans: Accessing funds for working capital, expansion, acquisitions, or operational expenses. This can include unsecured business loans, secured business loans, or lines of credit.

- Trade Finance: Solutions to facilitate international trade, such as letters of credit or debtor finance.

- Specialist Finance: Assisting with unique or “left-of-centre” scenarios, such as financing for newer businesses, those with complex financials, or specific industry needs, including low-doc equipment finance.

Finance brokers understand the intricacies of business financials, tax implications of various finance structures, and the eligibility criteria unique to commercial lending. For a more detailed look, you can consult our guide on business asset finance.

What is a Mortgage Broker?

A mortgage broker’s focus is squarely on property-backed lending. Their primary role is to help individuals and businesses secure finance for residential or commercial real estate. This includes navigating the complexities of home loans, investment property mortgages, and refinancing existing property debt.

The core services a mortgage broker provides are:

- Home Loans: Assisting individuals to purchase owner-occupied properties, comparing rates and terms from a panel of banks and non-bank lenders.

- Investment Property Loans: Helping clients finance residential investment properties, often advising on different loan structures like interest-only loans.

- Commercial Property Loans: While some mortgage brokers may touch on commercial property, their specialisation remains property-centric, focusing on the real estate asset rather than broader business operational finance.

- Refinancing: Helping clients switch existing home or investment loans to potentially secure better rates or terms. See our refinance options.

Mortgage brokers are experts in understanding serviceability, loan-to-value ratios, and the various fees and charges associated with property lending.

Key Differences: Finance Broker vs Mortgage Broker

The fundamental distinctions between a finance broker and a mortgage broker can be summarised as follows:

| Feature | Finance Broker (Commercial Finance Broker) | Mortgage Broker (Home Loan Broker) |

|---|---|---|

| **Primary Focus** | Business assets, working capital, commercial loans | Residential & commercial property loans |

| **Product Range** | Chattel mortgages, equipment loans, unsecured business loans, trade finance, invoice finance, vehicle finance | Home loans, investment property loans, refinancing, construction loans |

| **Lender Panel** | Major banks, specialist equipment financiers, non-bank business lenders, private lenders | Major banks, non-bank residential lenders |

| **Expertise** | Business financials, cash flow, tax implications of asset ownership, industry-specific lending | Property valuation, serviceability, LVRs, residential lending criteria |

| **Regulation** | Regulated by ASIC and AFCA (Australian Financial Complaints Authority) | Regulated by ASIC and AFCA |

This table provides general distinctions. Some individuals may hold both accreditations, but their primary specialisation and expertise will typically lean towards one area.

When to Engage Each Specialist

Choosing the right broker depends entirely on your financing objective:

- Engage a Finance Broker when: Your business needs funds for assets like vehicles, machinery, technology, or requires working capital, a business line of credit, or expansion finance that isn’t tied directly to real estate. If you’re looking for a chattel mortgage for a new delivery truck or a loan to purchase an excavator, a finance broker is your go-to expert. Comparison platforms like Loan Phone also provide direct access to a broad panel of specialist business lenders, often streamlining the process. For more on equipment loans, check out our guide.

- Engage a Mortgage Broker when: You are looking to purchase, refinance, or draw equity from residential property, or purchase a commercial property to occupy or invest in. Their deep knowledge of the property lending market is invaluable for these transactions.

How Loan Phone Bridges the Gap for Business Finance

At Loan Phone, we understand that businesses often need more than just a home loan. Our platform is specifically designed to help Australian business owners compare and secure a wide range of business finance solutions. We act as a specialist finance broker, leveraging technology to connect you with over 100 lenders, including major banks like CBA, NAB, and Westpac, as well as specialist equipment financiers and non-bank lenders.

Whether you need a chattel mortgage for a new vehicle, equipment finance for machinery, or a business loan for growth, our streamlined online comparison tool provides personalised options quickly. For complex scenarios, our team of specialist brokers provides expert human guidance, ensuring you get the right finance structure tailored to your business needs, even for “left-of-centre” applications such as earthmoving equipment finance.

Frequently Asked Questions

What is the primary difference between a finance broker and a mortgage broker? +

The primary difference is their specialisation: a finance broker focuses on business financing (equipment, working capital, commercial loans), while a mortgage broker specialises in property-backed loans (home loans, investment property loans). Their lender panels and product knowledge align with these distinct areas.

What types of finance can a finance broker help with? +

A finance broker can assist with a broad range of business finance products, including chattel mortgages, equipment loans, commercial hire purchase, unsecured business loans, working capital finance, and vehicle finance. They help businesses acquire assets and manage cash flow, such as truck finance.

Are finance brokers regulated in Australia? +

Yes, both finance brokers and mortgage brokers in Australia are regulated by the Australian Securities and Investments Commission (ASIC) under the National Consumer Credit Protection Act 2009. They are also members of the Australian Financial Complaints Authority (AFCA), providing an avenue for dispute resolution.

Can a mortgage broker assist with business finance? +

Generally, a mortgage broker's expertise is limited to property-backed finance. While some may have a basic understanding of related business finance, they typically lack the specialist knowledge, lender relationships, and product range of a dedicated finance broker. It's best to consult a specialist for business finance, such as for an ABN loan.

Why use a comparison platform for business finance? +

Using a comparison platform like Loan Phone allows businesses to access and compare a wide range of finance options from 100+ lenders simultaneously. This streamlines the process, potentially securing more competitive rates and terms for chattel mortgages, equipment finance, and business loans, often faster than going direct to individual banks. For example, you can compare chattel mortgage lenders.

Get Business Finance for Your Business

Ready to explore your business finance options?

Loan Phone combines streamlined online comparison with specialist broker expertise.

Fast Online Comparison - See personalised options from 100+ lenders

Specialist Support Available - Expert guidance when you need it

Efficient Processing - Streamlined process with digital document handling

Free, No Credit Impact - Use our comparison tool with no effect on your credit score

Related Resources

Explore these related guides for business owners and ABN holders:

Disclaimer: This article provides general information only and should not be relied upon as financial or tax advice. Rates, terms, and eligibility vary by lender and individual circumstances. Tax benefits are subject to your specific business structure and circumstances. Always seek independent professional advice from a qualified accountant and financial adviser before making financing decisions.

Loan Phone www.loanphone.com.au | loans@loanphone.com.au

Compare Loans Now - No impact to your credit score

Last updated: 2026-01-22